The Fed Cannot Stop Runaway Inflation

Nothing Stops this Train

Exploding government debt is taking over, forcing countries to lower interest rates and hike taxes not for the economy, but for the debt.

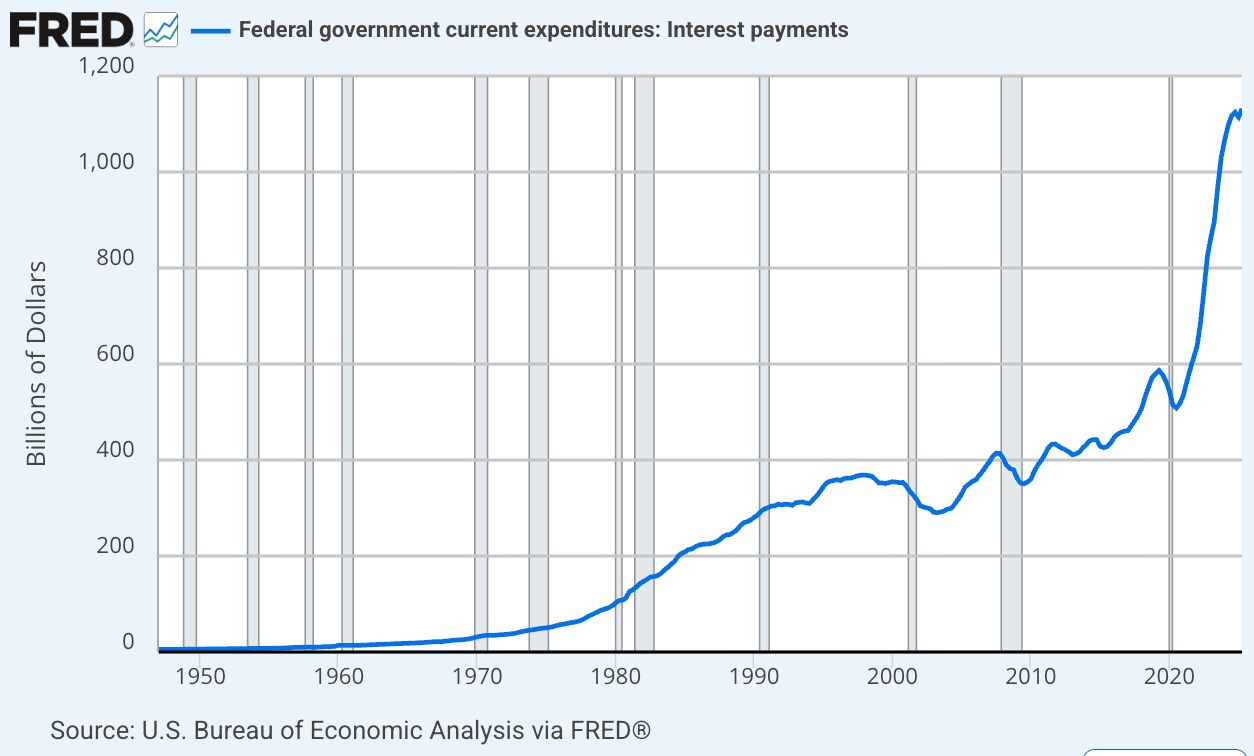

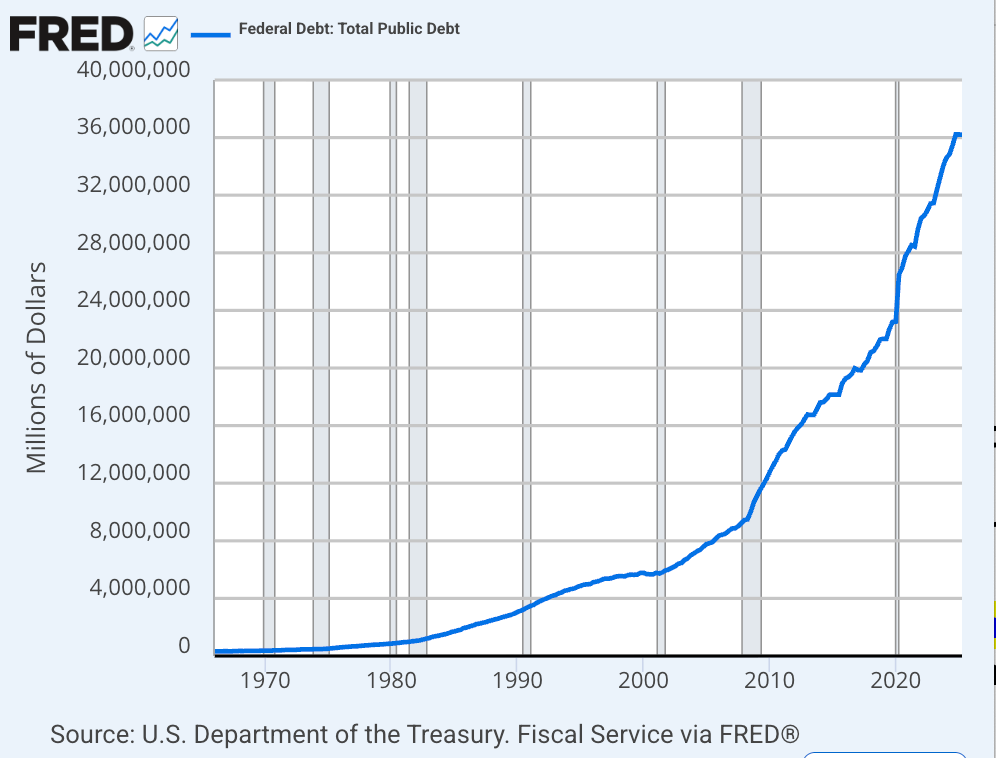

For months now Donald Trump has been hammering Jerome Powell to cut rates because of exploding interest payments on our $36 trillion national debt.

One tweet berated "Too Late Powell” for costing $360 billion per year for every point of interest rates.

Of course, that's just federal debt -- toss in state, local, and private debt and it's closer to $570 billion of additional debt payments for every point of interest rates.

Meanwhile, in Britain, the government just announced fresh tax hikes -- on top of the biggest tax hike in a generation -- to convince investors that Britain can actually handle deficits over 5 percent of GDP.

Note the US is actually worse -- we're over 6% deficit. But we have the world's reserve currency that Britain lost specifically because of out of control spending a hundred years ago.

I also mentioned in a recent article Japan's Prime Minister announced they can never again cut taxes. Because the debt is too big.

This all raises the specter of something called fiscal dominance, where debt gets so big that it takes over economic policy.

Meaning the Fed cannot raise rates -- and governments cannot cut taxes. In fact they're forced into tax hikes.

Fiscal Dominance

Fiscal dominance is a problem for a couple reasons.

First, it castrates central banks. Because when debt interest is large, rate hikes stimulate the economy — more money flows into the economy.

While cuts strangle the economy -- the debt payments go down.

This is the opposite of how it’s supposed to work. In other words, the debt cancels the Fed's tools.

Second, fiscal dominance forces long term inflation. Because central banks are forced into low rates and even money-printing -- “Quantitative Easing” -- to keep debt cheap enough for bond markets to absorb government deficits.

Third -- and most important — fiscal dominance means central banks cannot stop runaway inflation.

To see why, consider what happened in the 1970's inflation. At the time, there was concern central banks had terminally lost the plot and it was game over -- the dollar would collapse, millions wiped out, and we go back to gold.

But that didn't happen. Because Fed chair Paul Volcker jacked interest rates to 19% -- levels we hadn't seen since the Civil War hyperinflation.

19% rates gutted the economy, of course. But it stopped inflation in its tracks.

And it reassured bond investors that there is a 19% parachute if inflation hits the fan.

The problem is back in the 70's even adjusting for inflation the national debt was ten times smaller. Today it's 120% of GDP.

That means we cannot do the Volcker thing today. There is no parachute.

Why Volcker 2.0 is Impossible

To illustrate, the current deficit is around 2 trillion, of which half -- 1.1 trillion -- is debt interest.

If inflation got out of control and the Fed hiked to 19%, in the first year alone $10 trillion of debt has to be refinanced. It goes from 3% interest to 19% -- six times higher.

That alone adds an additional $1.5 trillion to the deficit — it goes to $3.5 trillion.

Give it another 2 years — and another $10 trillion of federal debt refinanced — and the deficit hits nearly $5 trillion.

$5 trillion is almost 20% of GDP.

There is no way investors are buying a 20% deficit. Countries like Turkey or Sri Lanka blow out at 10%.

Meaning the Fed has to step in as buyer of last resort, printing every last penny. Which makes the inflation worse.

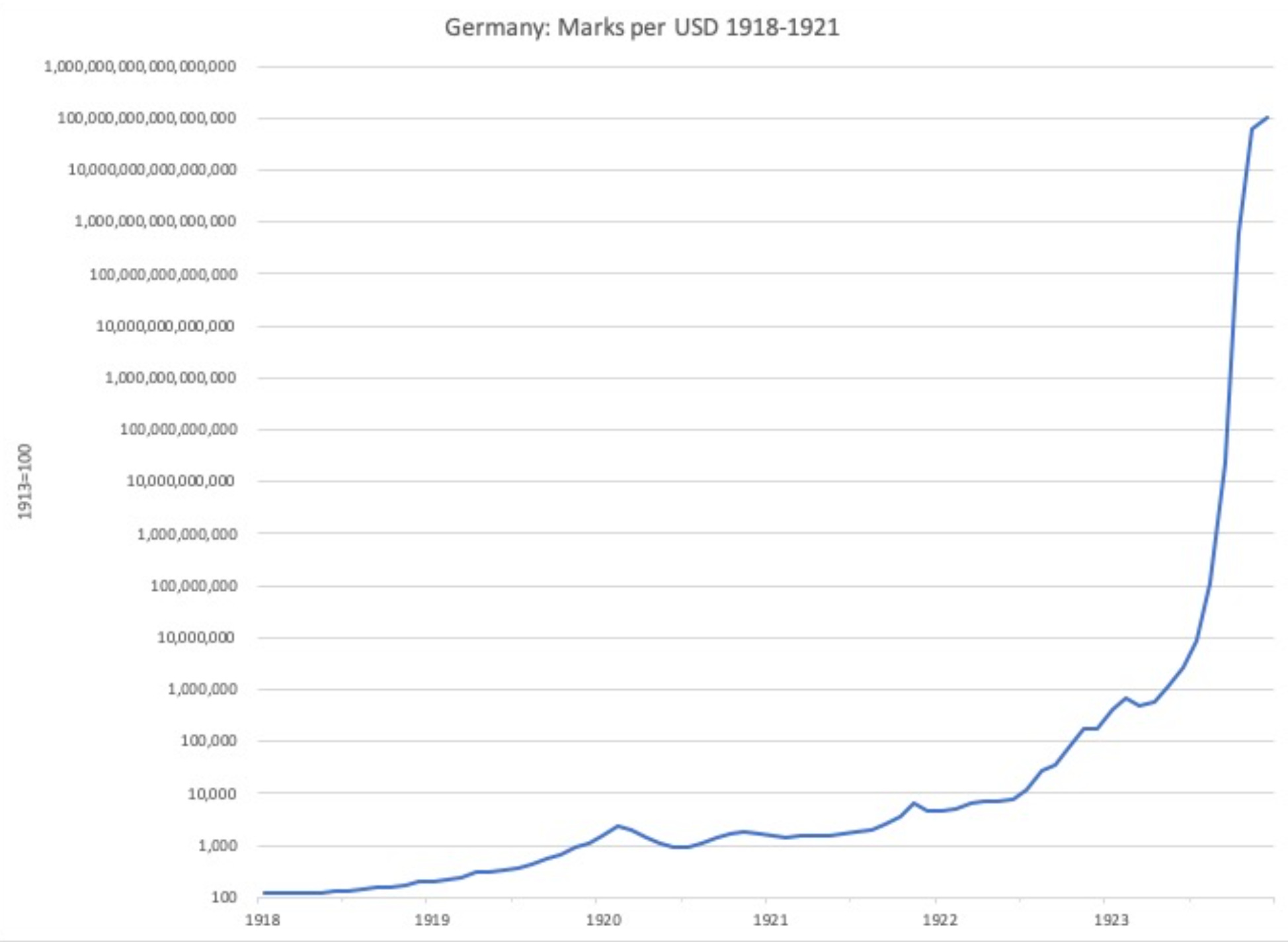

That’s the Weimar Germany solution: The Fed effectively prints the deficit.

At that point the Fed is fighting fire with gasoline. And inflation soars to 20 to 30%, maybe higher.

What’s Next

The Volcker parachute that backstopped the entire Ponzi for 50 years is gone. Congress spent it.

Absent a crisis, the dollar’s reserve currency status could buy another decade, even two, as foreigners absorb the fresh dollars. But our entire financial system is now flying without a parachute.

And when the next crisis does hit and inflation runs away again, the Fed will find their nuclear option has no fuse.

.

Every week I write a newsletter on the top stories in economics with regular deep dives into history like the Fall of Rome, the Weimar hyperinflation, or FDR’s Great Depression.

Subscribe for free, or choose $5 a month to access the comments section, over 50 archived articles, and help keep us on the air.

I also make short daily videos on economics and freedom:

20 minute Roundup Podcast of all the week’s videos: Search Peter St Onge on all major Podcast platforms

Lynn Alden said that. So what is your projection as to what comes after the fall of the US Dollar? How does the US evolve? How does the world trading system evolve?

What would happen if Congress got some fortitude and actually cut spending? I know its a fantasy but what would happen?