How the 1990's Balanced the Budget

What would it take to balance the budget. Does anything stop this train?

As the government shutdown eases in to its third week, odds are rising that the deficit could actually shrink from last year.

Perhaps by hundreds of billions if Republicans keep the shutdown going to the magic 61 days.

That’s the good news.

The bad news is even hundreds of billions barely makes a dent in a deficit that’s cruising at $2 trillion per year.

So what would it take to actually balance the books.

The 10th Amendment Solution

My inner Rothbard says it’s super easy: Defund every part of government that’s not authorized under the 10th amendment. Which says the federal government can only do what’s specifically listed — enumerated — in the Constitution.

That list -- in full -- is army and navy, courts and embassies, the post office, and minting gold and silver coins.

Everything else is unconstitutional -- yes, including the Fed.

That would give us a surplus of roughly $5.2 trillion.

Per year.

In the first decade use that $5.2 trillion annual surplus to buy out Social Security and Medicare with guaranteed annuities.

The second decade pay off the national debt.

Presto, you’re debt-free with a tiny 1913 style government.

The witch is dead.

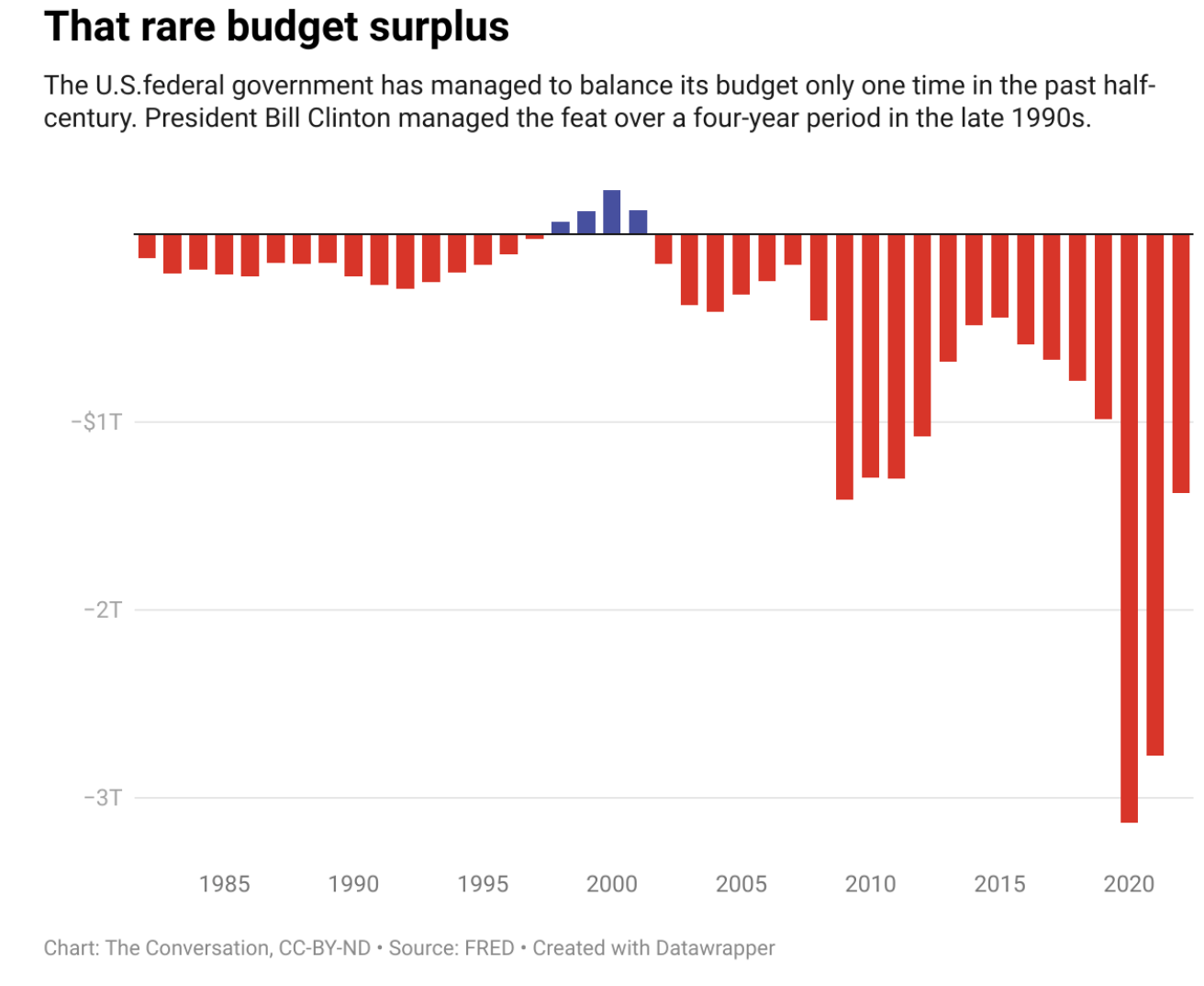

The 1990’s Balanced Budget

Of course, the odds on this happening are pretty low — Congress prefers keeping the $5.2 trillion.

In the real world, the last time we ran a surplus was in the 1990’s. In modern GDP terms turning a $1.1 trillion deficit in 1992 to a $700 billion surplus by the end of the decade.

A $2 trillion swing in just 8 years.

Sadly, the surplus lasted precisely 3 years until the combination of dot-com recession, medicare and medicaid expansion, and invasions of new and interesting countries plunged us back into the abyss.

Still, when a pig flies you don’t ask how many years.

How the 1990’s Balanced

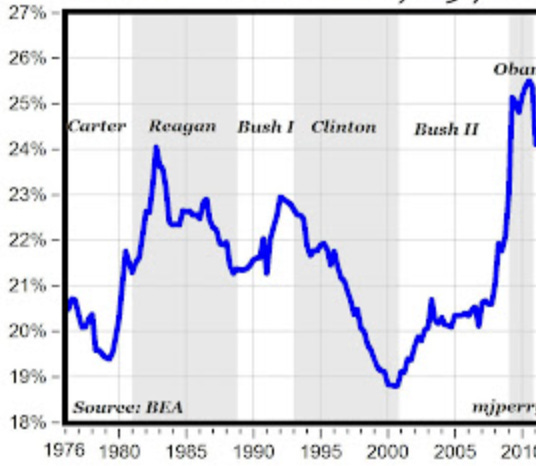

What drove the magical 90’s was 3 things: lower spending, the dot-com bubble, and a pair of budget mechanisms that forced Congress to limit spending.

On spending, Republican Newt Gingrich and Democrat Bill Clinton famously hated each other, so the uniparty was temporarily in civil war.

After a series of government shutdowns, they truced to essentially hold spending flat while the economy boomed. Which took spending as a percent of GDP down by nearly a quarter.

Roughly half of that was reduced military spending with the collapse of the Soviet Union — which Congress normally would have re-spent but instead held off.

The other half was genuine restraint.

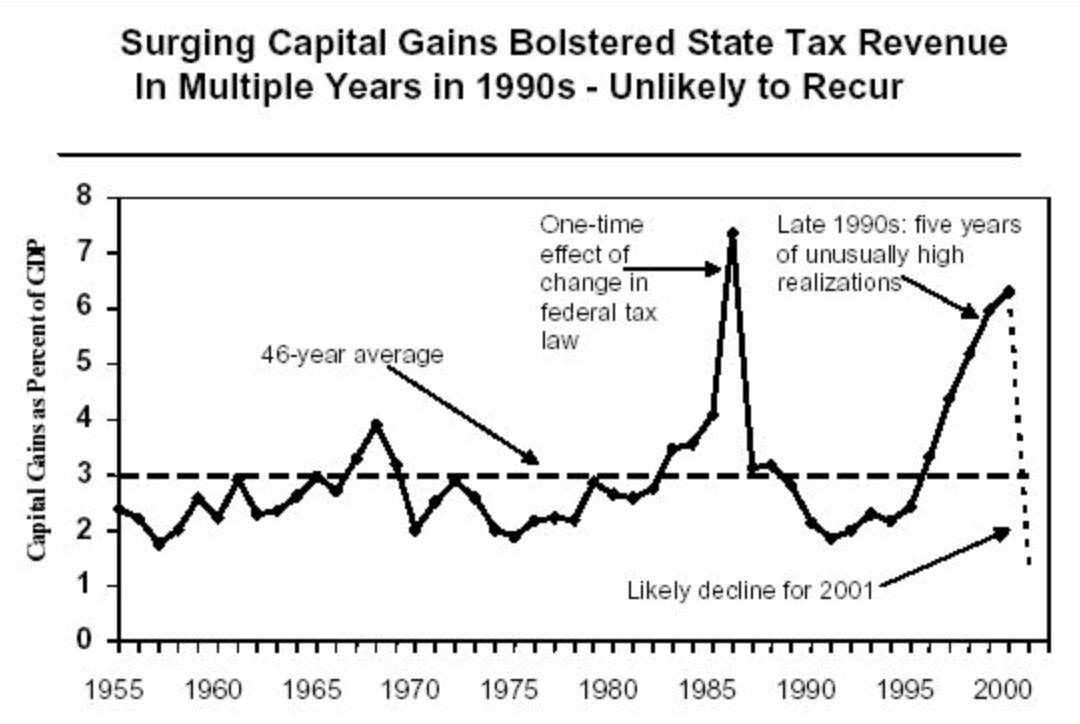

Next, taxes. Bush the elder and Clinton both raised income tax rates, but the higher rates didn’t raise revenue. This is the so-called Laffer Curve, where higher taxes make people work less, which lowers tax revenue.

Instead, it was the dot-com boom that hiked capital gains taxes by, in modern GDP terms, roughly a trillion dollars a year. Money that, again, the uniparty didn’t re-spend since they were at war.

Finally, two budget mechanisms that tied Congress’ hands.

So-called PAYGO, which requires new spending be paid in new taxes unless it’s an emergency.

And the Balanced Budget Act, which capped spending.

Both were gamed -- emergency took on fascinating new meanings. But both more or less worked until they expired in 2002 when Bush the Younger needed more wars.

What’s Next

It’s possible to balance the budget. But it needs two things: A uniparty at war -- as ours happily is at the moment.

And a president who doesn’t blow it on new pet projects.

Trump’s been relatively restrained so far — especially on war. But the jury’s still out whether Washington can keep their checkbook in their pants.

Every week I write an article on the top stories in economics with deep dives into history like the Fall of Rome, the Weimar hyperinflation, or FDR’s Great Depression.

Subscribe for free to get every article. Or choose $5 a month to access nearly 100 archived articles, the comments section, and help keep the lights on.

I also make short daily videos on economics and freedom:

20 minute Roundup Podcast of all the week’s videos: Search Peter St Onge on all major Podcast platforms