Private Credit Cracks

Echoes of 2008

Cracks are spreading in the $1.8 trillion dollar private credit industry. Echoing the 2008 financial crisis but this time gutting the load-bearing walls.

On Tuesday the Financial Times reported Ares Management, which runs $623 billion, limited redemptions in one of their flagship funds.

That’s the asset management equivalent of a bank run -- investors can’t pull their money because it could spark a fire sale that could collapse the whole fund.

For scale, $623 billion would make Ares the 9th largest bank in America -- just ahead of Capital One.

Spreading Cracks

Ares joins a rogues' gallery of funds that have locked redemptions, starting with Blue Owl which was managing just over $300 billion -- more than American Express -- before it did start fire sales.

During the Blue Owl drama, JPMorgan CEO Jamie Dimon warned when you see one cockroach there’s more. And they’re now coming every couple days: We’ve seen locks in Blackstone, Apollo, Cliffwater. Just last week Morgan Stanley capped redemptions at a major private income fund.

What’s driving it is what drives every bank panic: bailouts encouraged risk. Namely, since the 1990’s finance assumes it’ll a bail out from the Fed if things go bad.

The iron law of finance says more risk more profit -- you can charge more on a risky loan. So bankers do what bailouts pay them to do: Get rich or die trying.

On the ground, that meant hundreds of billions in loans to dodgy borrowers with sweetheart terms that let the borrower roll over the loan if they can’t pay -- so-called covenant-lite deals.

So borrow $100 million at 10%, and when you can’t pay the $10 million interest they just call it a $110 million loan and pretend everything’s fine. Known in the game as “extend and pretend.”

That hides the fact borrowers are in default. Because a loan in default might be worth 30 cents on the dollar. Or 5 cents. Like Enron but an assembly line.

The Fed’s Bait-and-Switch Hikes

Meanwhile, the Fed -- as always -- fed the fire with interest rates.

You’ll recall back in 2023 a clutch of banks went bust because their bonds were worth less after the Fed hiked rates for Bidenflation. Rate hikes lower bond prices, which left trillion dollar holes in bank balance sheets.

That happened on steroids to private credit, much of which went to commercial real estate that got double-hit with work from home and blue-city mismanagement that crushed office prices with vacancy rates hitting 40 year highs -- one in five offices is now empty.

Even more money went to dodgy corporate borrowers to fund leveraged buyouts that are now swimming in debt, like First Brands that went out last month with $12 billion in default. Sera Simmons, Citrix, and Envision may have doubled that.

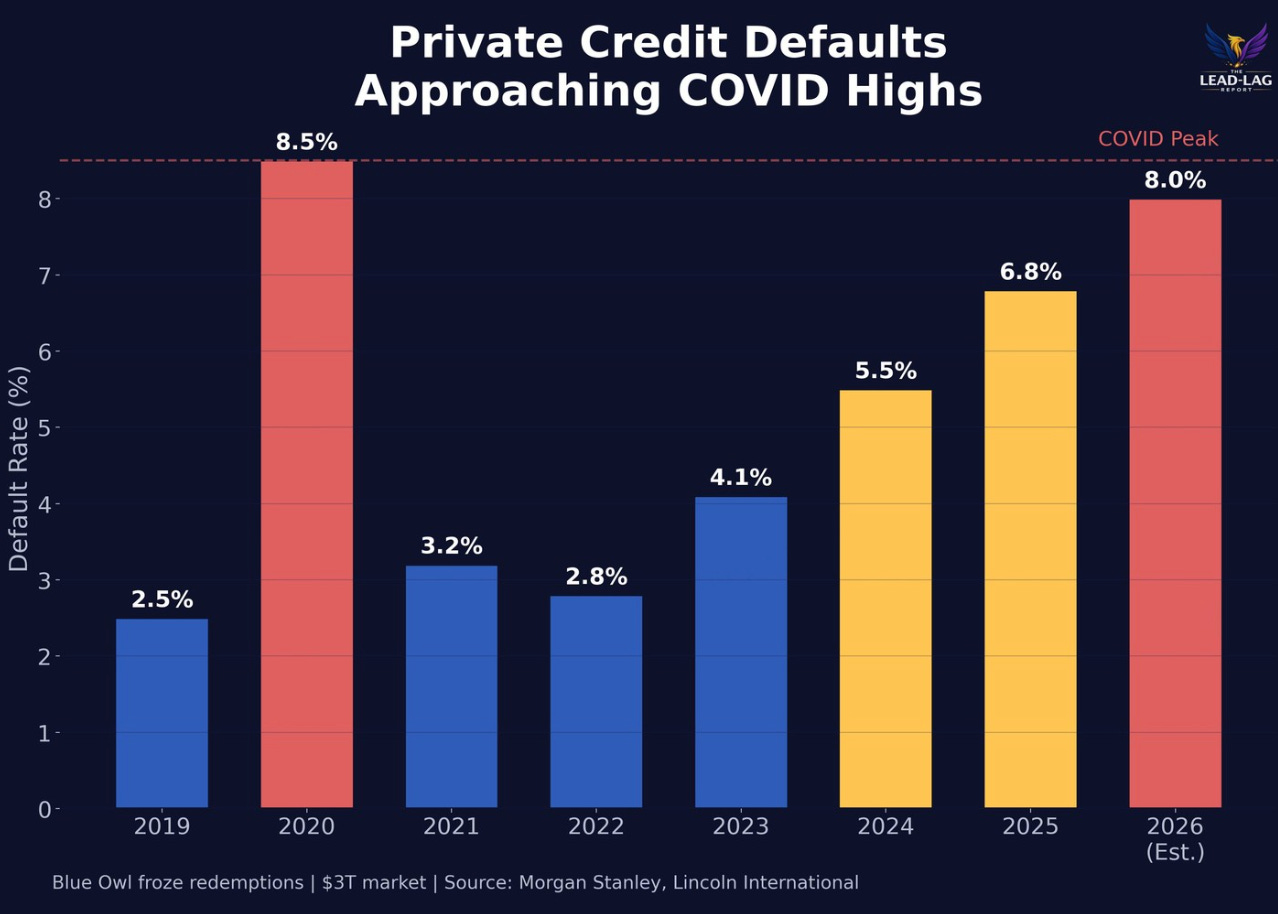

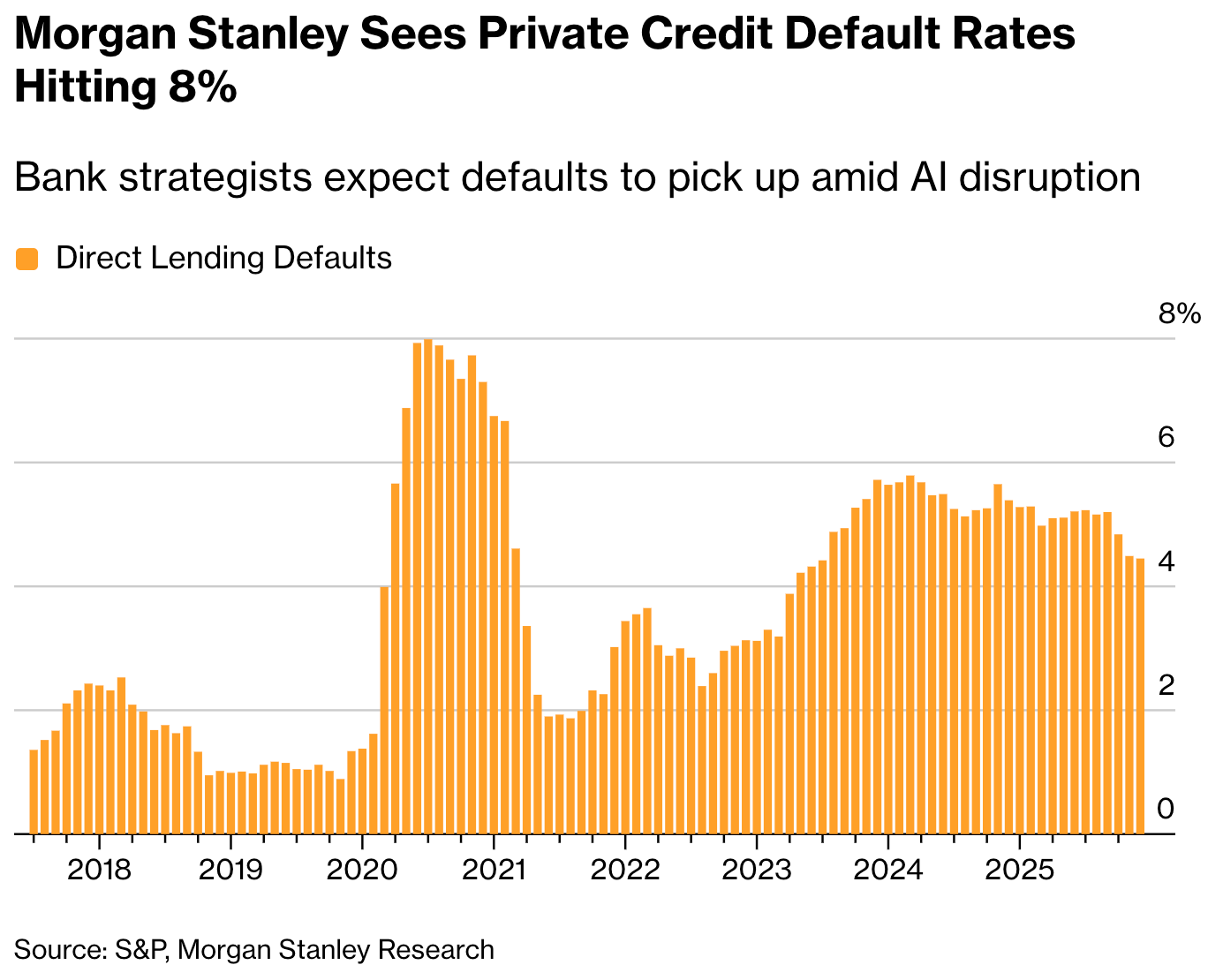

With potentially a lot more: Barclays estimates half of private credit loans are to software and business services that are getting gutted as AI gives it away for free.

The problem is when the loans go bad, investors get haircuts -- some get wiped out. That matters because nearly half of private credit money came from pensions and insurance companies.

If they can’t pay pensions or insurance claims that has bailout stamped on its head.

What’s Next

The Fed’s permanent bailout and interest rate adventures created a monster in private credit. Nobody knows how many cockroaches there are -- not surprising considering they’re hiding it.

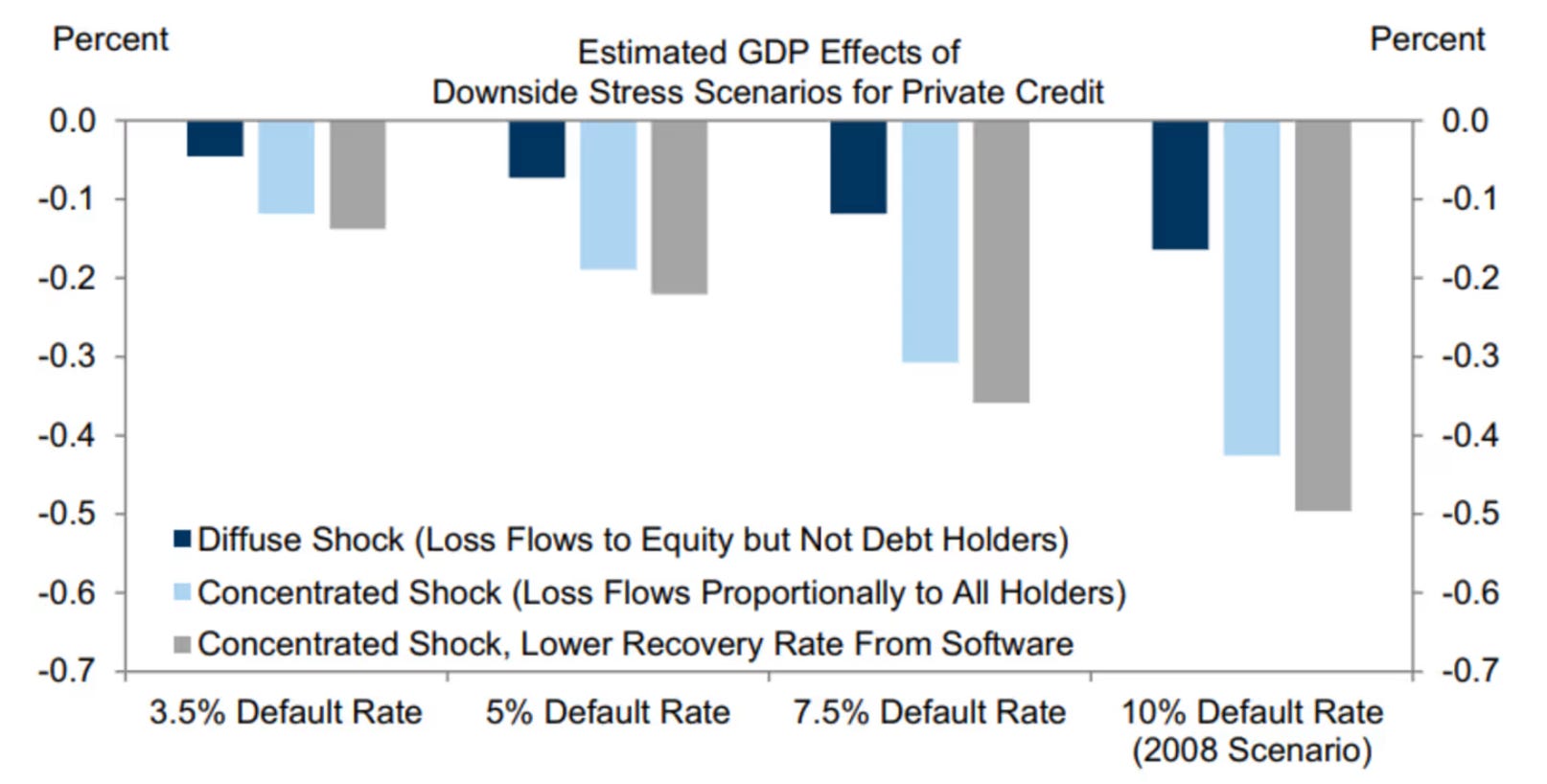

And if the Ponzi does collapses, you will pay it off -- as always, bankers eat their wins, you eat their losses. While GDP could take up to a half-point hit — representing about half a million jobs.

It’s not 2008 scale — yet.

But given the near-weekly blow-ups it could get big fast.

Every week I write on Economics and Freedom. Consider joining over 23,000 subscribers and becoming a free or paid subscriber to support my work.

I also make daily 3-minute videos on economics and freedom, also posted as videos on X.

And every week I gather these into a 20 minute Roundup Podcast that posts on all major platforms.

Thanks for reading!

One would think that these managers could foresee what is coming and act responsibly, however, when talking to the young bucks in the private equity business as well as the M&A folks in large corporations (typically Harvard and Wharton graduates), I am always stumped by their lack of real-life experience and their inability to think logically. They seem to think that life takes place in spreadsheets and have no interest, let alone knowledge, in the underlying products and processes that create the actual value. Or, as we used to say about economists, you can't talk about the macro if you don't know about the micro.

"Investors can’t pull their money because it could spark a fire sale that could collapse the whole fund". Curious why you didn't mention that most private credit Terms and Conditions don't allow random withdrawals. If investors want to play with the big dogs, they're responsible for knowing what they're getting into. 'Private' used to mean 'Private' ... for many reasons. Private Credit funds aren't EFT's !! As always, we've let too many children play adult games ...