Renters and Owners Living in Separate Economies

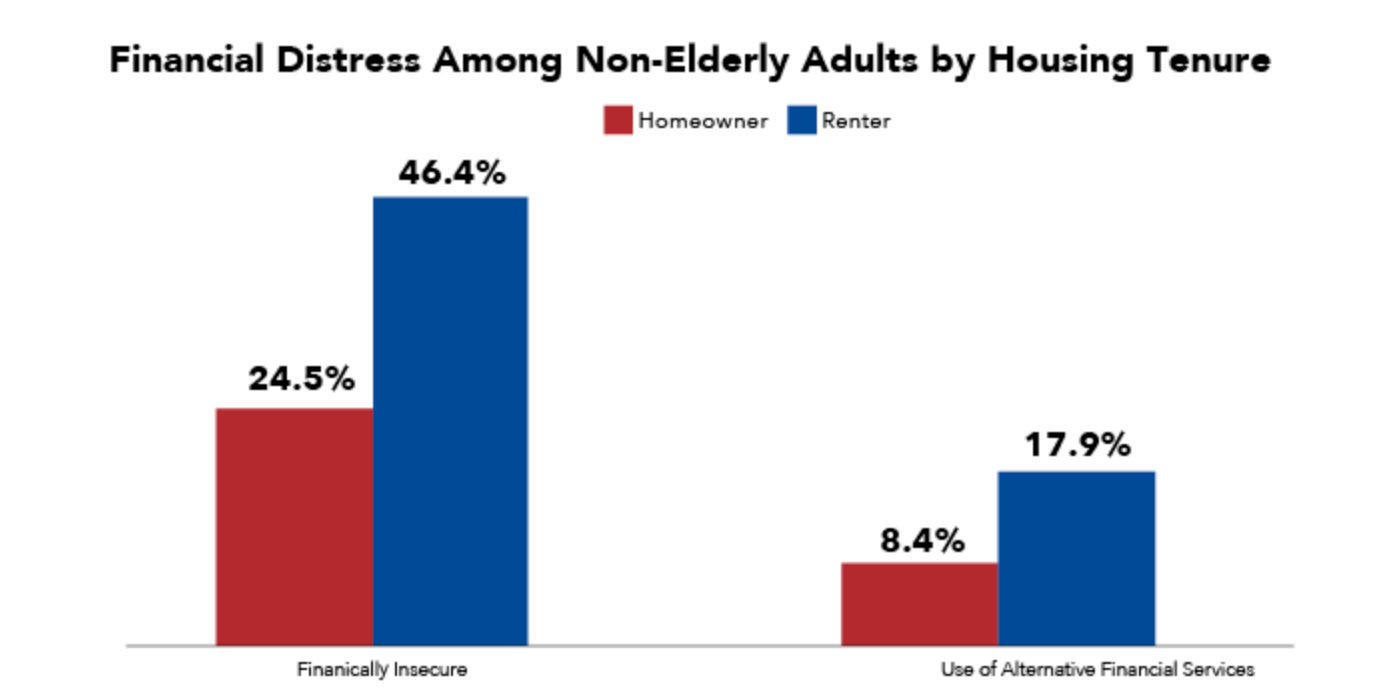

It turns out renters and homeowners are living in two entirely different economies, at least according to a new study by the Federal Reserve. Who, ironically enough, made it happen.

In short, renters are are in dire straits financially, while homeowners are "continuing to reap the rewards" of cheap pandemic money that left renters with nothing but inflat…