Will the Iran War Set Off a Recession?

Will the Iran War send us into recession?

Turning Donald Trump’s totally awesome 1980’s boom into a 1970’s quagmire?

As soon as the bombs started falling over Teheran, American markets crashed. Bonds fell. Silver plunged. Even gold is down.

Oil, of course, jumped from $67 to $75 per barrel.

Oil Disruption

Markets always react fast to war – and they can over-react. The question for the real economy is how long does this war last.

This is because the main impact is oil prices. And these are driven by supply disruptions from the Middle East.

About one-fifth of oil exports pass Iran’s Strait of Hormuz. Another third are in range of Iranian missiles.

The US actually imports almost none of this Middle Eastern oil – it’s just 2% of our consumption. But oil prices are global so what happens in Iran does not stay in Iran

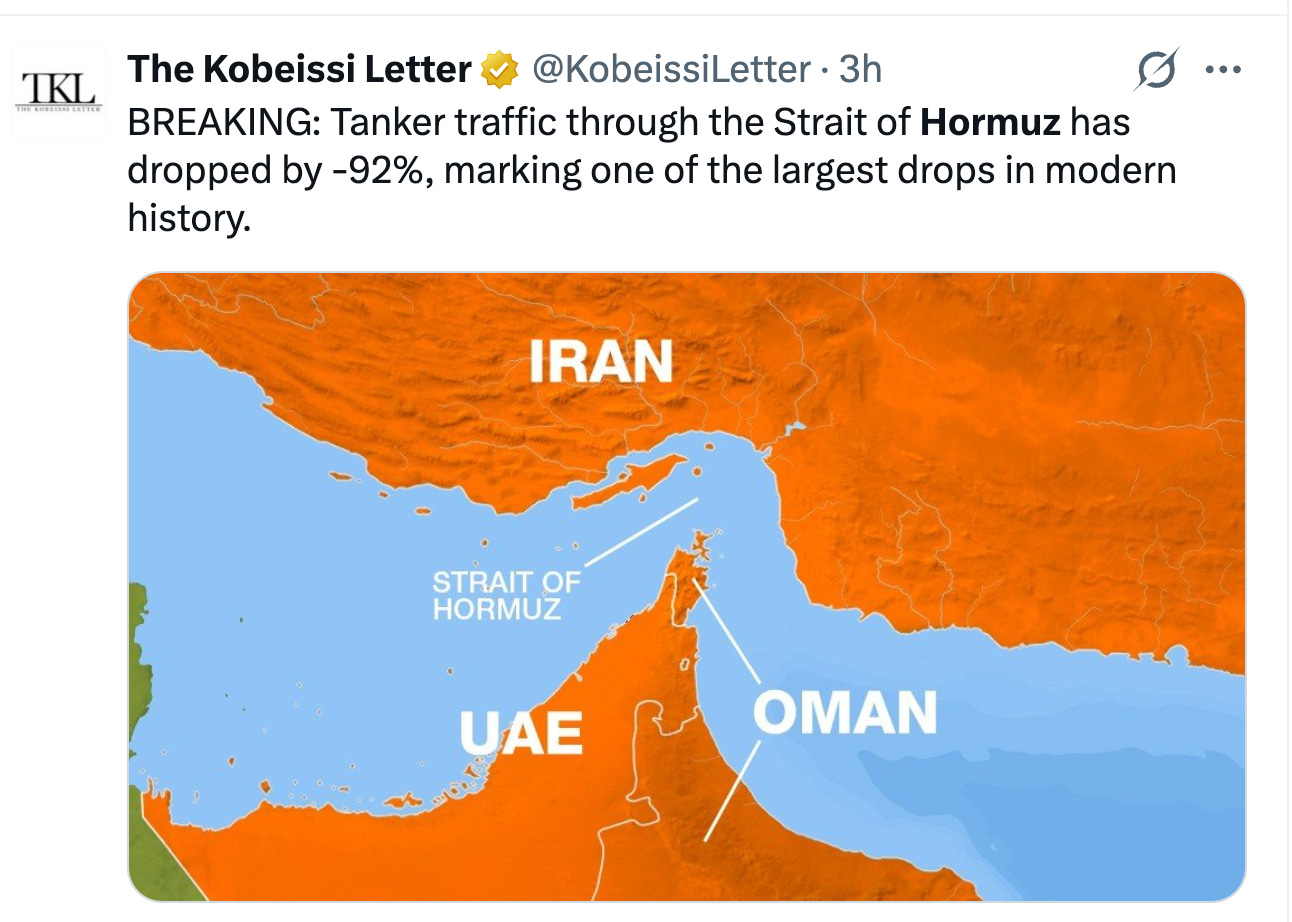

On the day bombs started, ship traffic in the Strait of Hormuz fell 70%. Within 3 days it ground to a “total halt.”

Trump responded with government guarantees on ship insurance, which helps. But traffic won’t recover until the bombs stop. So it’s a question of how long the bombs continue.

Trump is currently promising the war will last just 4 weeks. But the administration is also messaging it will go “as long as it takes.”

You do that to demoralize the other guy. But it means this is not a one night stand like Venezuela or last time Trump bombed Iran.

Iran’s Impact on the Economy

There’s 3 key baskets of economic fallout: Growth. Jobs. And inflation.

Historically every $10 rise in oil knocks about two-tenths of a percent off economic growth. That’s small in an economy that’s growing over 3% -- it lowers wage growth by about $200 per year.

But it goes on top of expensive oil to heat your home or gas your car. A $10 jump translates into 25 cents a gallon of gas. Together with heating and trucking raises household costs another $300 a year.

And it bumps inflation by up to a third of a percent.

Next, expensive oil and growth both hit job creation -- $10 might drop job creation by 10 to 15 thousand per month.

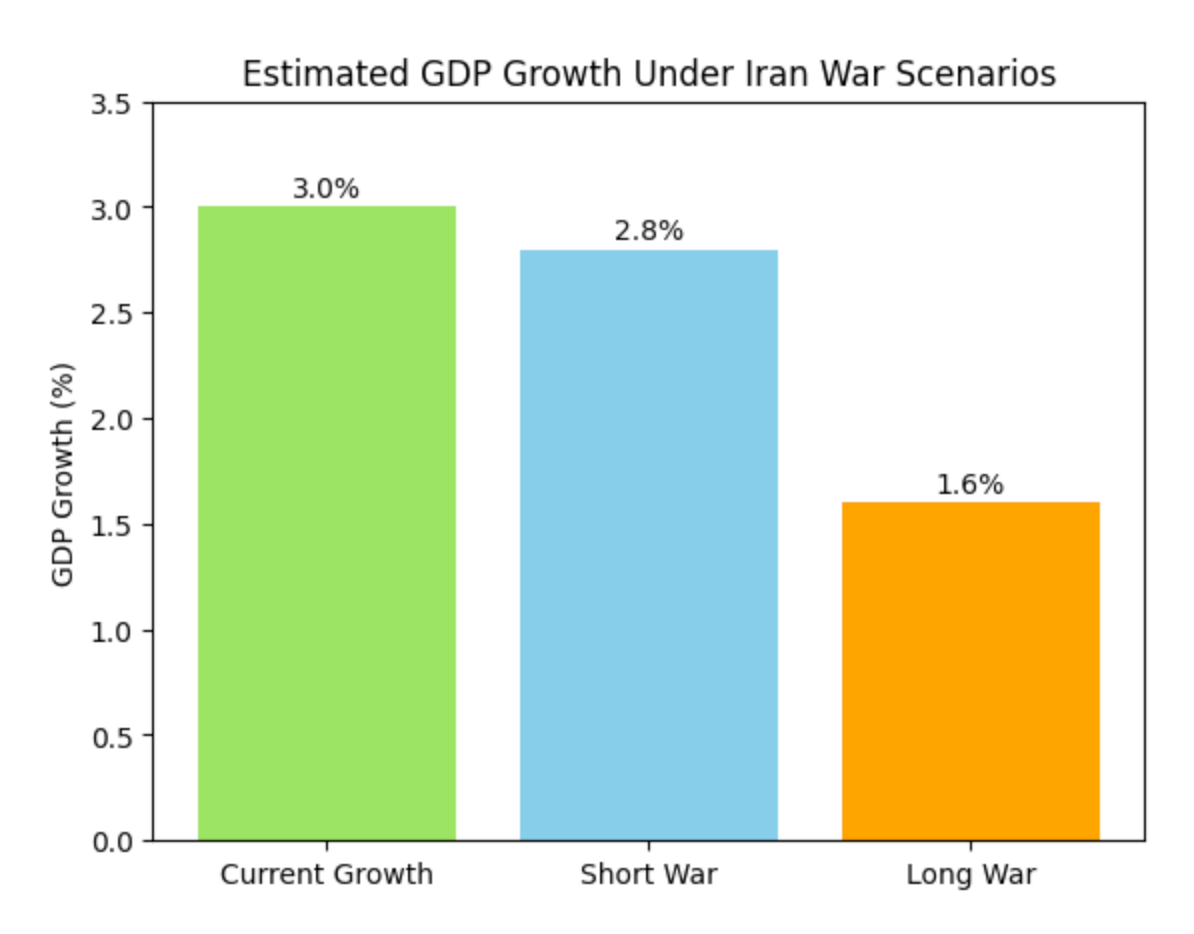

All this is painful. But it’s not recession. What would put us in recession is a long war.

A recent study by Deutsche bank looked at historic oil shocks, concluding you need a 50 to 100% ongoing jump in oil to set off a recession.

This would imply oil prices of $100 to $150 — on a sustained basis, not just a spike.

The good news is, according to Deutsche, even at $100 — or $150 — oil only causes recession when you’re already limping.

The 1970’s is the poster-child for an oil crash. But we were already in bad shape thanks to Washington’s so-called guns and butter policy of dumping trillions into the welfare state while ramping up the Vietnam War.

It’s important to note the Nixon Shock and lost decade kicked off long before the oil embargo.

In contrast, today we’re growing at 3 percent according to FedNow. Productivity is soaring 4.9% -- one of the highest since the Reagan boom.

So oil could knock us into the 1% to 1.5% on growth. But it won’t set off a recession unless the Fed panics on oil prices and hikes rates. Which could mow down millions of jobs.

What’s Next

For now the war’s biggest impact is oil prices.

But if it keeps going those cascade into growth, jobs, and inflation.

At which point Donald Trump could throw away his hard-earned boom just in time for Midterm elections.

Each week I write on Economics and Freedom. Consider joining over 22,000 subscribers and becoming a free or paid subscriber to support my work.

Every day I also make 3-minute videos on economics and freedom, also posted as videos on X and on Rumble. Every week I gather these into a 20 minute Roundup Podcast, search Peter St Onge on all major podcast platforms.

Peter,

Your piece correctly identifies the Deutsche Bank threshold: $100-150 sustained oil only causes a recession when you're already limping. But I'd push back on the implication that we're not already limping.

The private equity complex was deteriorating well before the first bomb fell. Carlyle and Blue Owl have seen significant drawdowns over recent weeks, not war casualties, but pre-existing credit stress. In 2007, PE drawdowns preceded the Bear Stearns moment by several months. The oil shock gets the headline; the credit impairment is the actual mechanism. The setup right now looks similar: illiquid assets marked above market, leverage stacked throughout the capital structure, and a refinancing environment that gets harder every month. If PE marks start cascading and credit spreads widen, your oil math changes substantially. We're no longer starting from 3% growth; we're starting from something already impaired.

Second point, and I think this one's underappreciated: at this stage of the credit cycle, an oil spike may be deflationary rather than inflationary. The speed of the move matters more than the absolute level. 2008 is the better analog. Oil spiked to $147 in July, then crashed to $35 by December as credit seized. The initial spike looked inflationary; the aftermath was deflationary collapse. If the Fed reads the early oil move as inflationary and holds rates, they could be tightening into a credit contraction. That's the scenario that turns pain into severe pain.

The 1970s required guns-and-butter fiscal profligacy as the foundation. 2007-2008 had a credit system quietly failing before anyone declared a crisis. The second analog fits better here.