Regional Banks Crash on "Cockroach" Loans

Fears of hidden losses at regional banks sent them skidding last week with potentially hundreds of billions of bad loans.

Is your neighborhood bank a hedge fund in disguise.

This is a big deal because regional banks hold roughly 1 in 4 deposits in the US -- about $5 trilion.

And they account for half of all industrial and commercial loans — and 80% of mortgage loans. Because big banks prefer lending to foreign countries, hedge funds, and the US government.

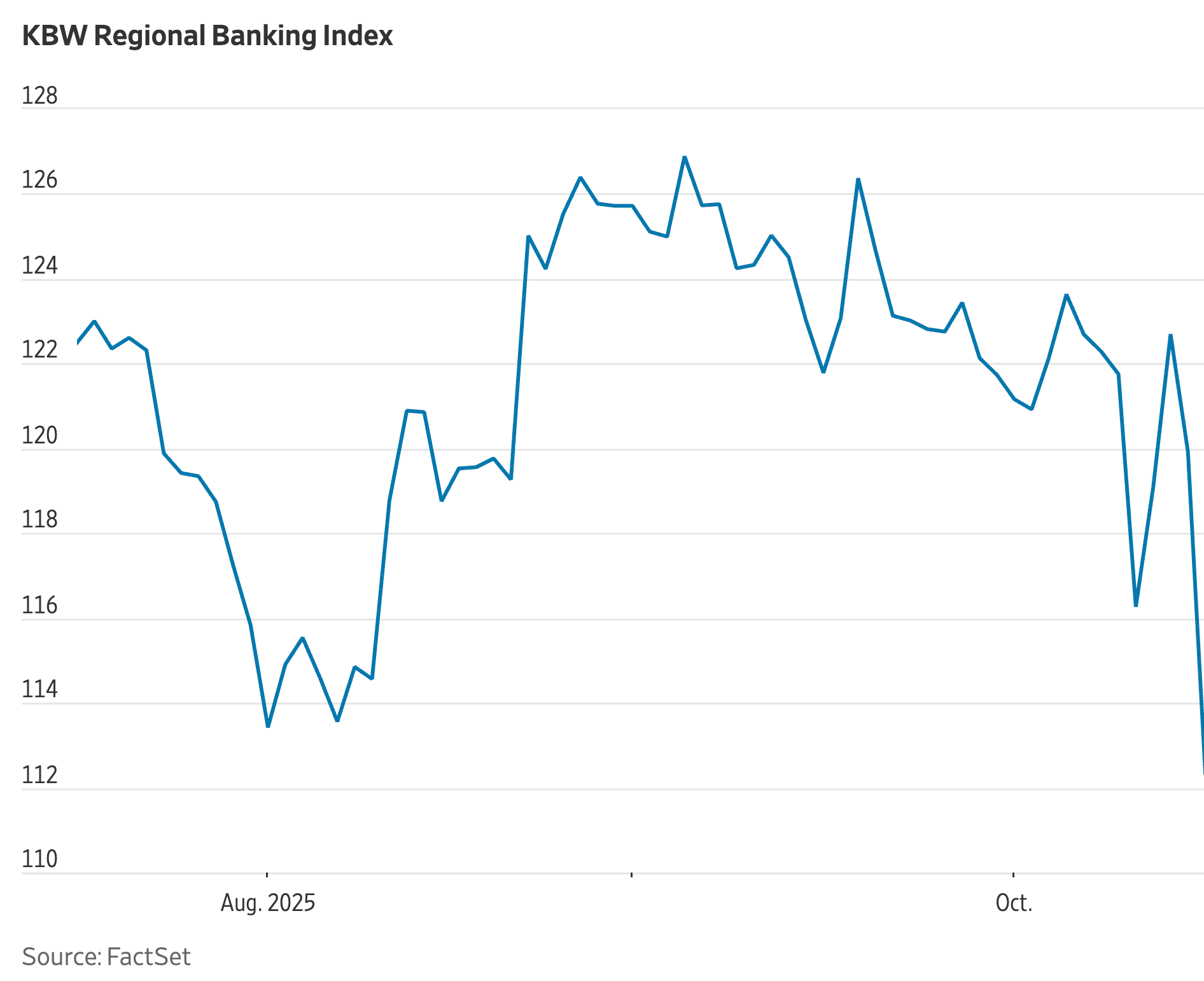

Regional Banks Crash

The trigger was the bankruptcy of First Brands, an apparent $6 billion ponzi-scheme that bought up boring car parts makers, borrowed heavily against them. And blew up with at least $2.5 billion vanished.

Calling into question First Brands’ other $10 billion of loans.

The blowup sent investment bank Jeffries crashing 9% in a single day.

And it follows another auto lender that blew up last month with a $170 million dollar hole.

Meanwhile, separate disclosures from a pair of large regionals piled on.

Zions Bancorp fell nearly 20% after announcing it discovered 2 big commercial loans with “apparent misrepresentations.”

Western Alliance fell 11% in a single day after disclosing it’s suing a major borrower for fraud.

Together, these 3 account for nearly a quarter trillion in assets. And they took the entire regional banking industry down 6% in a single day as investors wonder if anybody’s actually looking at these loans.

Or if they’re just cutting checks to anybody in a suit. As JP Morgan’s Jamie Dimon put it, “when you see one cockroach there are probably more.”

Regional Banks’ House of Cards

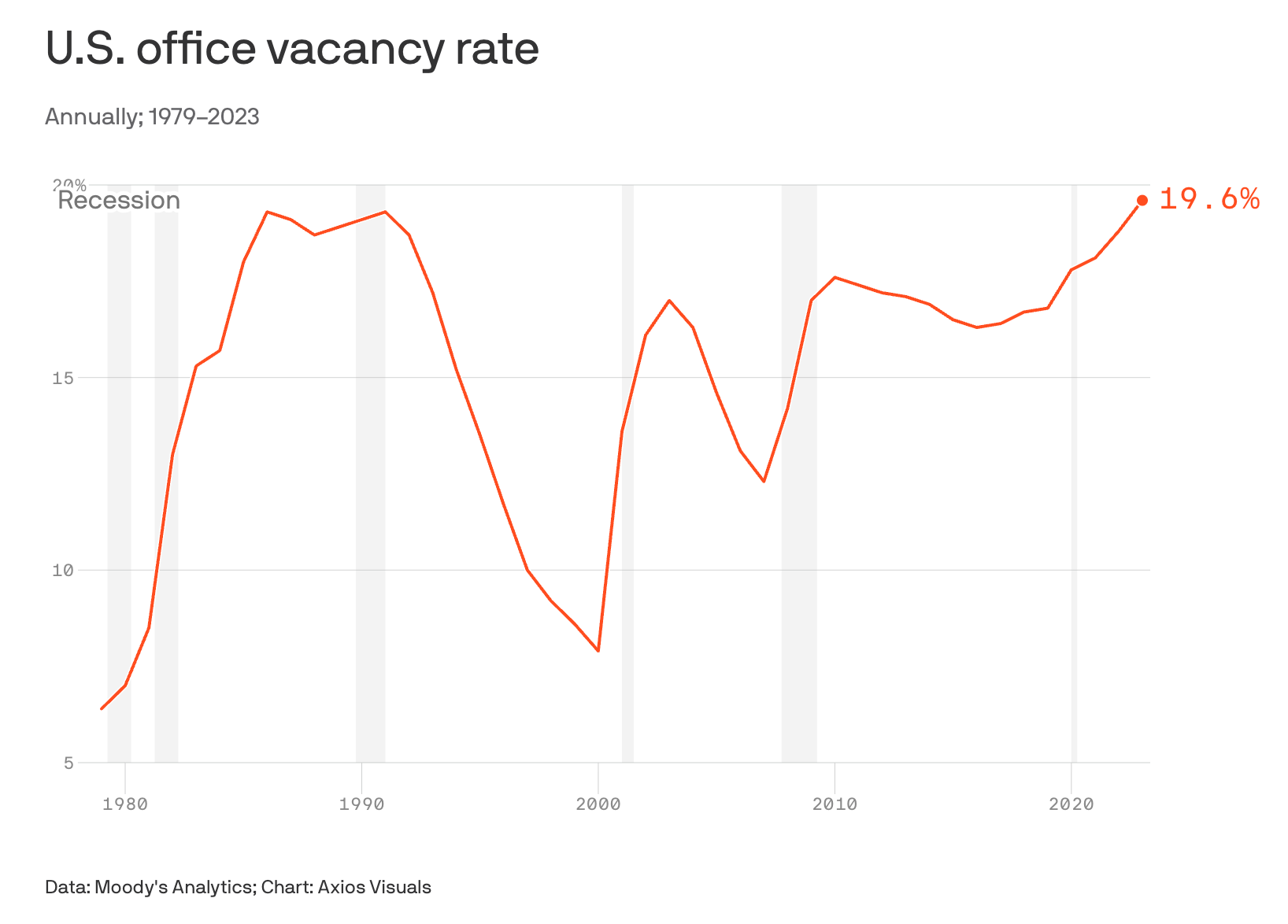

Regional banks were already sitting on land-mines in the crashing commercial real estate sector, with office vacancy rates hitting a record 20% -- in 2019 it was 12%.

According to Morgan Stanley, there’s 18 years of supply sitting empty for Class-A offices, and 23 years for lower-grade Class-B.

Meanwhile 7% of commercial real estate is in delinquincy. Despite banks gaming it with so-called extend and pretend, where the bank keeps lending to failed projects to make the loan appear healthy.

Fraud if you do it. Standard practice in banking.

This matters because commercial real estate makes up nearly 44% of regional bank assets.

So if the industrial loans are also garbage there’s not much left.

It’s worth remembering regional banks nearly imploded just 2 years ago, with a cascade of bank failures that actually exceeded the 2008 crisis until the Fed and Treasury stepped in with a series of bailouts.

These included $30 billion in write-offs -- which are taxed from your bank account. $200 billion in sweetheart loans against fictitious asset values. And Janet Yellen promising to cover $20 trillion of deposits with just $100 billion at the FDIC.

200 to 1 leverage.

Even hedge funds wouldn’t dream of that.

What’s Next

Regional banks may be in dire straights. And some could go bust.

But it won’t take down the economy for the simple reason that banks used the 2008 crisis to institutionalize bailouts -- call them pre-bailouts.

That’s how we got 2023; banks no longer have to go through the humiliation of asking for bailouts, they get them without lifting a finger. Fictitious asset loans and all.

Bailouts make banks risky, and regionals have the cockroches to prove it.

So expect more bad loans.

And expect a whole lot more taxpayer bailouts.

.

Every week I write an article on Economics and Freedom here on Prof St Onge Weekly.

Subscribe to get each article in your inbox — choose Free if money is tight, or choose $5 a month to help keep the lights on.

I also make short daily videos on economics and freedom:

20 minute Roundup Podcast of all the week’s videos: Search Peter St Onge on all major Podcast platforms